Manias In Plain Sight

The AI frenzy has evolved from a sector trade into a full-blown macro mania, driving extreme positioning, speculative flows, and global short & medium term earnings expectations to historic highs.

In the last few years since covid it seems there has always been some sort of mania afoot in the financial markets, ranging from Gamestop to gold.

While each specific target of the mania always has its own fundamental narrative, drawn throughout all of these is the combination of a) monetary policy that remains easy enough to keep the overall system lubricated to allow money to chase the next hot target and b) a broad shift by many investors from medium to long-term views to short-term speculation.

In each case anyone who expresses prudence are considered sidelined fools who don’t get it - even at the level of book some gains and take risk off the table vs. chase the hot trade. But in most cases coming in once the hot trade has become well known is a recipe for losses ahead, just like it always has been since Newton’s time.

Markets over the last 6 weeks or so have surged on the AI/Semi optimism. $SMH was up 60% from the end of March bottom to the nearby top earlier this week. While those folks who have chased the rally make fundamental cases for why the surge in pricing is justified, it’s hard to make any compelling common sense case that the fundamental outlook has changed so much, so shortly for a sector of such size.

And that’s the difference between this mania and some of the ones of the recent past. It’s one thing to bid a single stock. Even spot gold is a pretty tiny market all things considered, where even a 10 or 20 billion incremental bid from the $100tln equity markets can create a squeeze. It’s a whole other dynamic to expect *global* equity earnings to surge 10% on the back of the sector at the center of speculation.

The mania is now macro, driving outsized stock market moves at the index level, not just the asset one. Everywhere you look within the pricing, incremental flow, or earnings expectations, what we are seeing today is extraordinary in any historical context. And as it grows larger it takes more and more capital to push pricing to even more extremes.

A Look At the Data

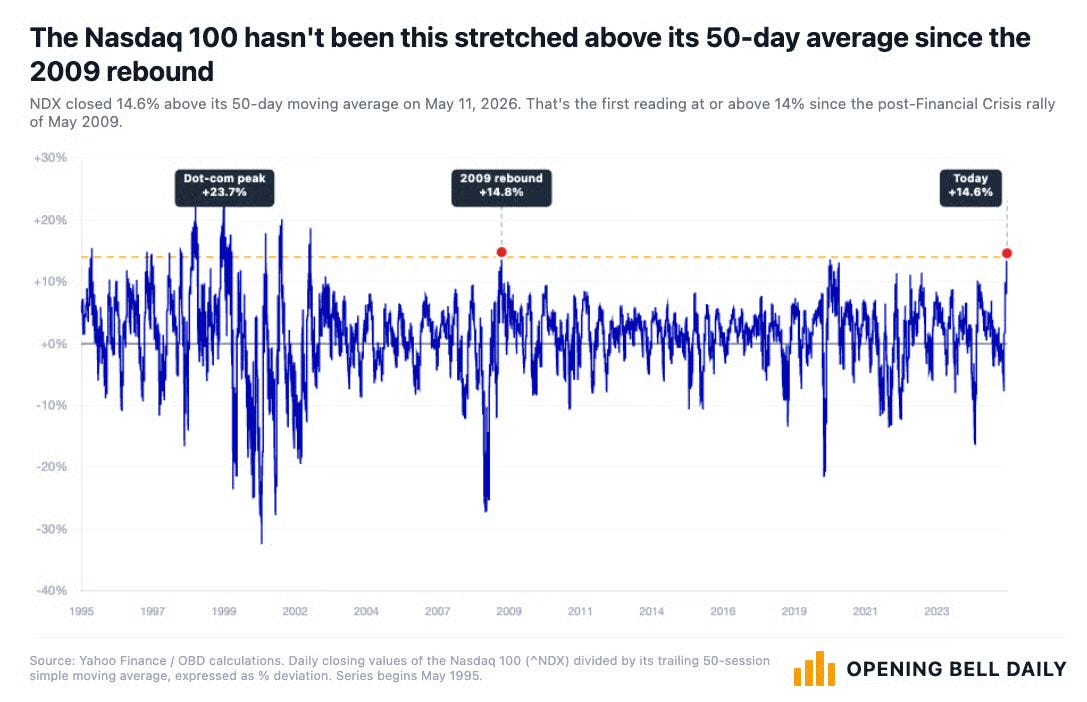

The last 6 weeks have seen a remarkable rally across markets, with the Nasdaq a good representative example, now running at extreme highs vs. its 50d average.

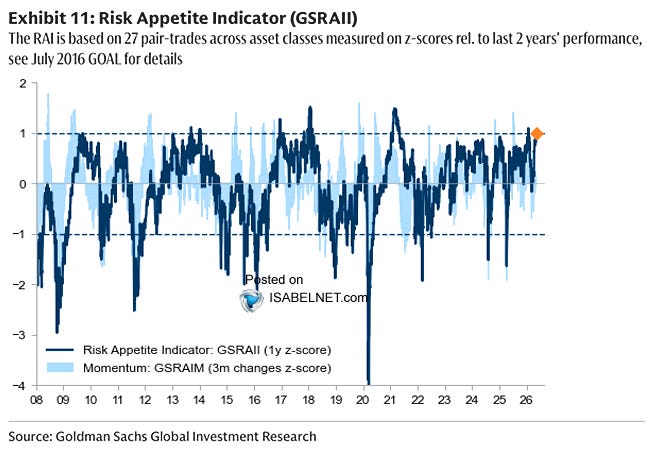

While it’s always hard to get a sense of how stretched the market is beyond just looking at the headline pricing, there are several internals pointing to extreme positioning relative to history. Goldman has an internal risk appetite gauge that is basically at all time highs of the last couple decades.

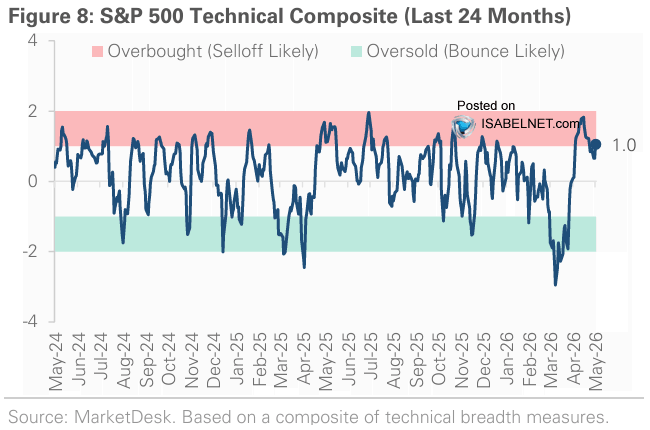

Shorter-term technical indicators are also pointing overbought.

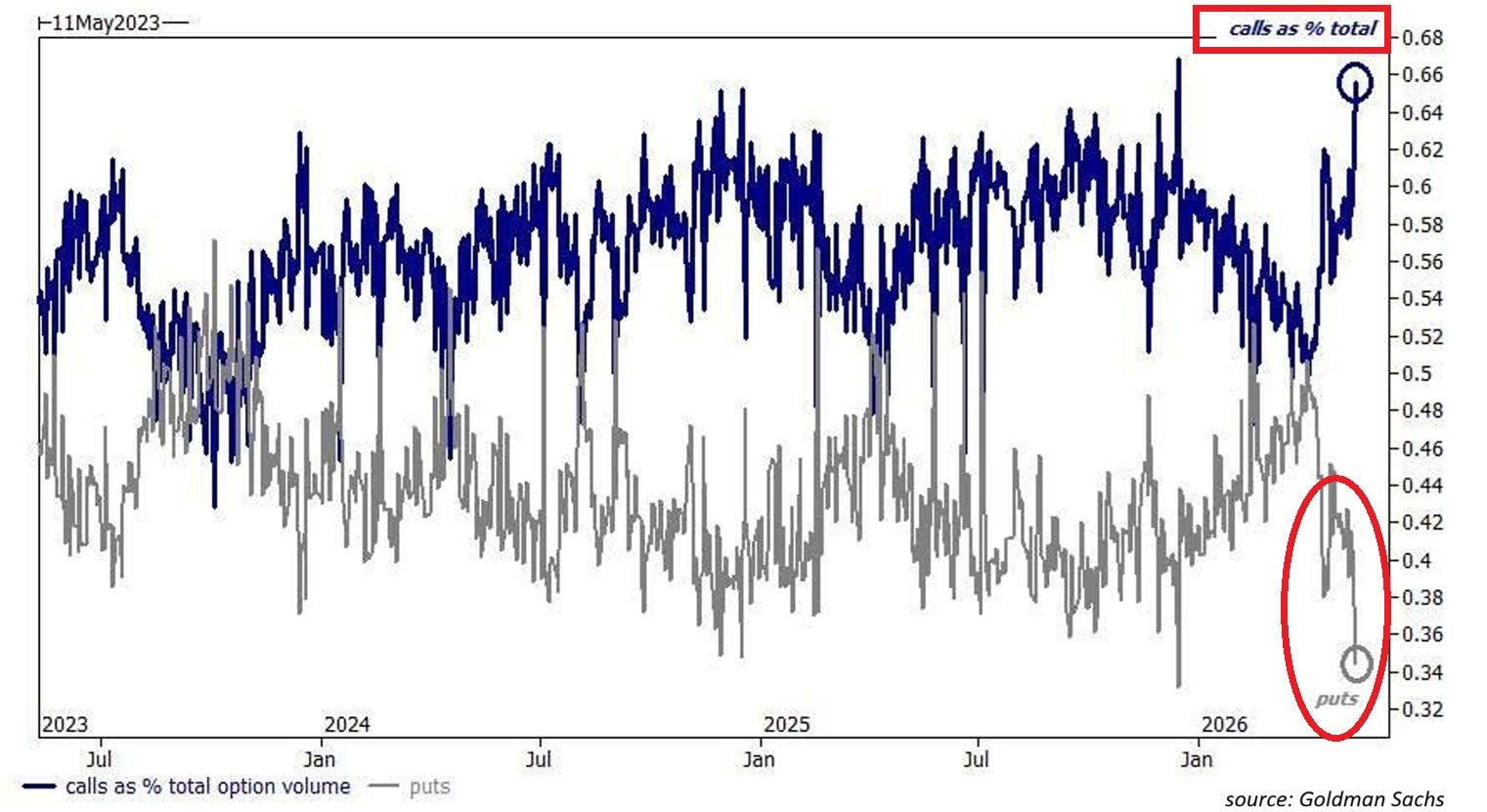

And the surge in call buying relative to puts suggests a surge in efforts to chase the right tail from a macro perspective.

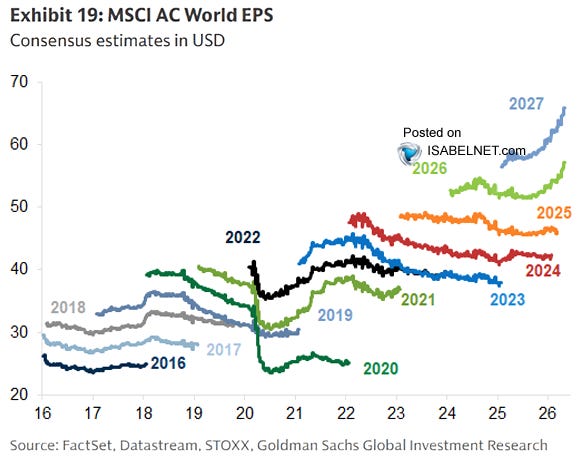

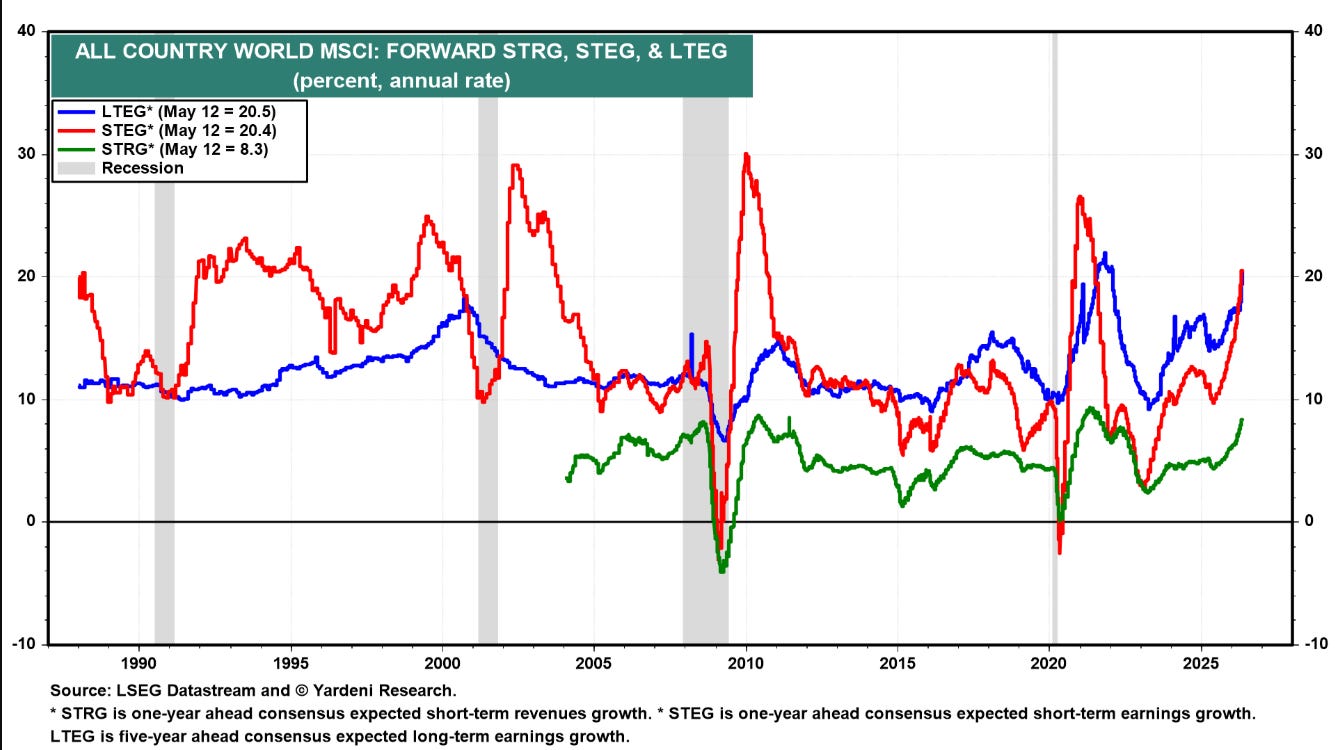

But it’s not just in the pricing and the flows. Analyst expectations are surging, fueling optimism at a macro level for these names. Since the start of the year ‘27 earnings expectations have surged nearly 15%, in sharp contrast to the typical downward revision trend that typically occurs. These shifts are highly concentrated in the AI/Semis names.

At this point the analyst mania grows along with market mania, we now have a situation where short-term earnings growth is now expected to be the strongest in decades outside of acute post-recession recovery periods. And long-term earnings growth is expected to be at its highest level in >40 yrs, and probably ever, outside the post-covid shutdown rebound.

Bottom Line

We’ve seen manias over the last few years on specific assets or sectors, but this current dynamic is now large enough that its now driven total market flow dynamics to extremes and global earnings expectations to extraordinary levels.

While it always feels like the talk of a luddite to question such extreme hopes, those who have studied the history of markets know that when these sorts of dynamics emerge it’s much more likely that it does not end well than reflects a near immediate radical remaking of the global economy.

Curious if you have a base-case valuation framework or target range for the S&P here.

I’ve been thinking through scenarios anchored to prior drawdowns — particularly the 2022 Russia/Ukraine inflation shock and the 4Q23 rate-driven correction tied to long-end yields and big tech earnings concerns.

A ~15% drawdown from current levels would roughly bring the market back toward 2023 valuation territory on forward earnings.

Wondering whether you view this more as a valuation reset regime or something that could evolve into a true earnings revision cycle. I can’t recall if you have written on that recently.

Hey Bob, appreciate the great work day in and day out. An un related question - your preference here: cash earning 3.7% or 20 year tips at 2.7%? thank you very much.